Budgeting is a crucial skill for managing finances effectively. It involves tracking income and expenses, setting financial goals, and making adjustments to achieve those goals. Whether you're trying to escape the paycheck to paycheck cycle, build up your savings, or just gain more clarity over your financial life, creating a budget is the first and smartest move you can make. Here's a detailed guide on how to budget money, along with resources to help you put each step into action.

Steps to Budget Money

Record Your Income

Before you can control where your money goes, you need to understand exactly how much is coming in. Start by documenting every source of income, this includes your main job, side hustles , freelance gigs, rental income, government benefits, dividends, or any regular financial support. Don’t just note the total amount, be specific about the frequency (weekly, biweekly, monthly) and whether the amount fluctuates.

If your income varies from month to month, take an average of the past 3 – 6 months to set a baseline. This clarity helps you plan your spending with confidence and ensures you’re not budgeting based on guesses or overly optimistic projections. Remember: your income is the foundation of your budget, get it right, and everything else has a solid place to stand on.

Add Up Your Expenses

Once you've mapped out your income, it’s time to face the reality of your spending. Start by gathering all the data, pull up recent bank statements, credit card bills, receipts and even mobile payment histories. You’re not just looking for big ticket items, it’s the $5 daily coffees and random online purchases that sneak up on you.

Break your expenses into three core categories:

- Fixed Expenses: These are the non-negotiables, rent or mortgage payments, utilities, insurance premiums, subscriptions, and phone bills. They typically stay the same month to month.

- Debt Expenses: Include minimum payments on credit cards , student loans, car loans, and any personal loans. These are vital to track because they impact both your cash flow and long-term financial health.

- Unexpected Expenses: These are the curveballs, car repairs, emergency travel, medical bills, home maintenance. While you can’t always predict them, looking at past transactions can help you spot patterns and create a buffer.

The goal here is accuracy. Don’t estimate, track. Use budgeting templates , spreadsheets, or budgeting apps to categorize your spending. You’ll likely be surprised by where your money has been going. And that awareness? It’s pure power.

Set Your Spending Limit

Now that you know how much you earn and where it all goes, it’s time to define what’s left: your disposable income. This is the money you have left over after covering all essential and fixed expenses.

To calculate it:

- Add up your total income for the month.

- Subtract your fixed and necessary expenses (including debt payments and an average for unexpected costs).

What’s left is your discretionary cash, the funds available for dining out, hobbies, shopping, streaming services, and anything else that makes life enjoyable but isn’t essential .

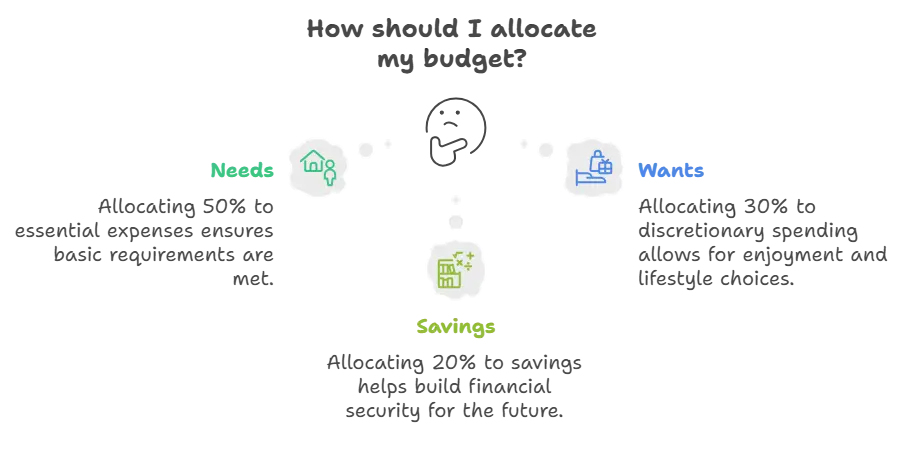

Here’s the trick: give every dollar a job . Decide upfront how much you'll allow yourself to spend in each discretionary category. Tools like the 50/30/20 rule (50% needs, 30% wants, 20% savings) can help you create balance, but feel free to tweak the ratios to suit your life.

Without a spending limit, money tends to vanish. With one, you create intention, and with intention comes control.

Set Your Savings Goal

A budget without savings is like a car without brakes, sure, you can move forward, but you’re not protected when life takes a sudden turn. That’s why setting a clear, meaningful savings goal is essential.

Start by asking yourself: What am I saving for? Your goal could be short term (a vacation, a new phone), medium term (a car, a wedding), or long term (buying a home, early retirement). Even something as practical as an emergency fund, a financial safety net of 3 to 6 months’ worth of expenses, should be on your radar.

Once you’ve defined the “why,” focus on the “how.” Determine a realistic monthly savings target based on your disposable income. If your goal is to save $1,200 in a year, that’s $100 per month. Keep it specific, measurable, and time-bound.

Prioritize savings like it’s a bill, non-negotiable. Consider setting up automatic transfers to your savings account the moment your paycheck hits. Out of sight, out of temptation. The earlier you start, the stronger the habit. And the stronger the habit, the more unstoppable your financial growth becomes.

Adjust Your Budget

A budget isn’t meant to be written in stone, it’s a living, breathing reflection of your life. As your circumstances evolve, so should your budget.

Did you get a raise? Add a new monthly subscription? Pay off a loan? Maybe your grocery bill jumped, or you’re spending more on transportation. All of these shifts require a budget check in.

Make it a monthly ritual, grab a coffee, open your financial tracker, and review:

- Did you stick to your limits?

- Did any unexpected costs pop up?

- Can you increase your savings or need to cut back in certain areas?

This is where flexibility meets accountability. Adjust your allocations based on real life, not just ideal numbers. The goal isn’t perfection, it’s progress. When you revisit your budget consistently, you build financial resilience and confidence that can carry you through whatever comes next.

Budgeting isn’t one big decision . It’s a thousand small adjustments made with intention. Keep refining. Keep improving. Keep moving forward.

Make Budgeting Easier

Let’s be honest, budgeting can feel like a chore. But the right tools and systems can make it almost effortless. Think of it like fitness: if you have the right gear, a plan, and a bit of automation, showing up gets a lot easier.

Start by separating your bank accounts. A simple three account system works wonders:

- One for bills and essentials

- One for everyday spending

One for savings

This separation creates clarity. You’ll instantly know what’s safe to spend versus what needs to stay untouched.

Next, automate your finances . Set up direct debits for fixed bills, rent, utilities, loan payment, so they’re handled before you even think about them. Then, schedule automatic transfers to your savings account right after payday. This “pay yourself first” method removes the temptation to spend what you should be saving.

Use budgeting apps to track spending in real time. Tools like YNAB, Goodbudget , PocketGuard, or even your bank’s built in budgeting features can categorize expenses, send alerts, and visualize your money habits.

Finally, simplify your system to match your lifestyle. If you’re more analog, try the envelope method with physical cash or printable trackers. If you're a spreadsheet lover, build a custom Google Sheet. The best system is the one you’ll actually stick to.

Bottom line: Make budgeting seamless, not stressful. With a few smart moves, you’ll turn budgeting from a burden into a habit that runs on autopilot, and still puts you in control.

Budgeting Methods

There’s no one size fits all when it comes to budgeting. The best method is the one that fits your mindset, money habits, and lifestyle. Below are three popular approaches, each with its own vibe, benefits, and best-use scenarios. Whether you’re hands-on, goal-driven, or need a tactile reminder not to overspend, there's a system for you.

Zero Based Budgeting

Zero based budgeting is like giving every dollar a purpose. At the start of each month, you assign your income across various categories, spending, saving, bills, debt, until your total equals zero . This doesn’t mean you’ve spent everything; it means everything has been accounted for .

Example:

If you earn $3,000 this month:

- $1,200 for rent

- $400 for groceries

- $300 for savings

- $200 for debt

- $150 for transportation

- $150 for entertainment

- $600 for everything else

Total = $3,000

There’s no “leftover” money that can vanish into impulse buys, every dollar has a job.

Pros:

- Super intentional and transparent

- Great for detail oriented people

- Helps identify unnecessary spending

Cons:

- Can be time consuming to maintain

- May feel restrictive if you prefer flexibility

Best for: People who want complete control and are willing to track regularly.

Pay Yourself First Budgeting

This method flips the script: you prioritize savings and debt repayment before anything else . The idea is to treat your financial goals like non-negotiable bills, automatically taking care of them before spending on wants or even some needs.

Example:

If you bring in $2,500 a month and aim to save 20% and put 10% toward debt:

- $500 goes straight to savings

- $250 to credit card payments

- The remaining $1,750 covers everything else

Pros:

- Forces you to save consistently

- Helps build wealth and crush debt fast

- Automates discipline, set it and forget it

Cons:

- You need to be realistic about how much you can commit

- Can feel tight if income is irregular or expenses are high

Best for: People with clear goals who want to grow savings or reduce debt fast.

Envelope Budgeting

This is old school, and it still works. With envelope budgeting, you use physical envelopes filled with cash for specific spending categories (like groceries, dining out, or gas). Once the envelope is empty, that’s it for the month.

Example:

- $300 in your “Groceries” envelope

- $100 in “Entertainment”

- $50 in “Coffee & Snacks”

When the cash runs out, you stop spending in that category, simple and powerful.

Pros:

- Excellent for visual, tactile learners

- Prevents overspending by setting hard limits

- Builds real awareness around spending habits

Cons:

- Not convenient for online purchases

- Handling cash may not suit everyone

Best for: People trying to rein in impulsive spending or looking to reset their relationship with money.

Each method has its strengths. Try one, or a mix, to see what sticks. The goal isn’t just to budget, it’s to build a money system that works for you.

Budgeting Tools and Resources

A great budget is only as good as the tools behind it. Whether you're a tech savvy money tracker or someone who thrives on a printable spreadsheet, having the right resources can take the stress out of managing your finances and make budgeting feel less like a chore, and more like a game you’re winning. Here are some of the top tools to get you started.

Budgeting Apps

YNAB (You Need A Budget)

A cult favorite for a reason, YNAB is built around the zero based budgeting philosophy. Every dollar gets assigned a job, and you actively plan your spending ahead of time, not reactively. It’s detailed, hands on, and offers powerful reporting features to track your financial progress.

Best For: Budgeting nerds, goal setters, and those who want total control.

Strengths: Syncs with your bank, offers educational content, and encourages proactive financial planning.

Goodbudget

Think of Goodbudget as a digital version of the envelope system. You allocate “virtual envelopes” for different categories and manually log your spending. The app doesn’t link to your bank accounts, which helps users stay mindful and engaged.

Best For: Couples, cash based budgeters, or anyone who loves the envelope method without the physical cash.

Strengths: Shared household budgeting, intuitive interface, promotes conscious spending.

EveryDollar

Created by Dave Ramsey’s team, EveryDollar is another zero based budgeting app, but with a lighter touch than YNAB. The free version is manual entry, while the premium version allows for bank syncing.

Best For: Simplicity seekers and fans of the Ramsey method.

Strengths: Clean design, straightforward setup, great for beginners.

PocketGuard

PocketGuard is perfect for people who want a “big picture” look without getting too deep in the weeds. It links to your accounts and automatically shows how much money is safe to spend after accounting for bills, goals, and savings.

Best For: Busy individuals who want budgeting made simple.

Strengths: Easy to use, automated tracking, real time “what’s left” snapshot.

Financial Planning Resources

Looking to level up beyond the app? These resources provide practical, often free, tools to help you build your budgeting muscles:

- Moneysmart.gov.au Budget Planner : Interactive calculator for building your budget step by step.

- Canada.ca Budgeting Tools : Worksheets, guides, and budget calculators designed by government financial experts.

- NerdWallet’s Budget Templates : Downloadable Google Sheets and Excel tools to get started quickly.

- SmartAsset Financial Planning Resources : Includes articles, calculators, and tools for long-term planning.

- Better Money Habits by Bank of America : Offers videos, articles, and step by step guides for building smarter money habits.

- Local Workshops and Financial Advisors: Check with local credit unions, nonprofits, or community centers many offer free or low cost financial literacy classes and one on one coaching.