Understanding commercial loan terms is crucial for business owners seeking funding for growth, operations, or real estate. Whether you're expanding into a new market, purchasing equipment, or refinancing property, knowing how commercial loans work puts you in the driver’s seat.

Below is a comprehensive overview of the most common commercial loan types, structures, and key terminology every business owner should know before signing on the dotted line.

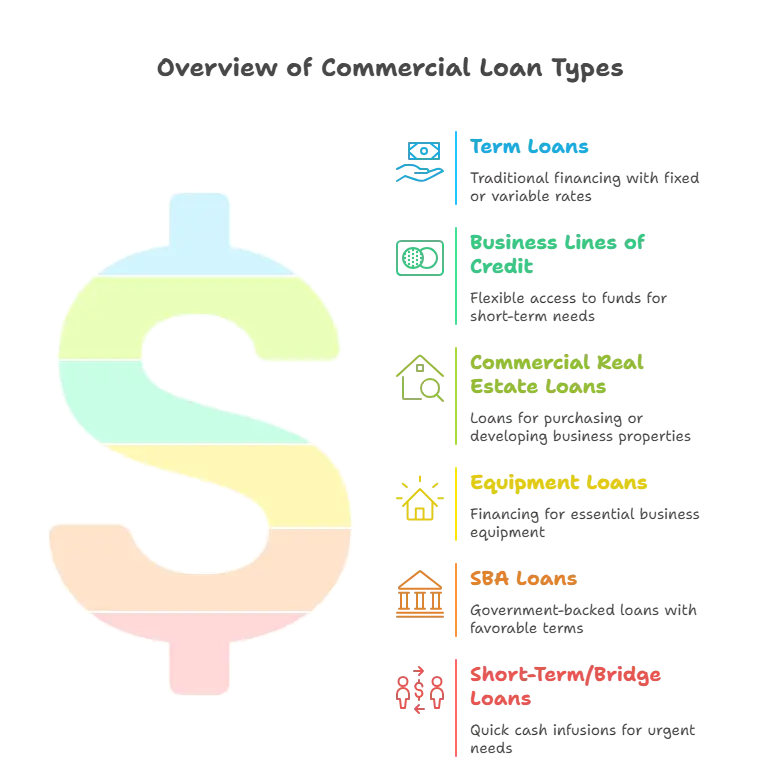

Types of Commercial Loans

Term Loans

A term loan is one of the most traditional and straightforward forms of business financing. It provides a lump sum of cash upfront, which you repay over a set period, typically ranging from 1 to 10 years. In some cases, especially for large real estate purchases, terms can stretch up to 25 years.

Interest rates may be fixed, offering predictable payments, or variable, fluctuating with market conditions.

Best for: Major purchases, business expansion, equipment upgrades, or debt consolidation.

Business Lines of Credit

Think of a business line of credit as a financial safety net. Instead of receiving one lump sum, you get access to a pool of funds you can draw from as needed, only paying interest on the amount you use.

Terms usually range from 6 months to 5 years, offering maximum flexibility for short term needs.

Best for: Managing cash flow gaps, covering unexpected expenses, or seizing sudden business opportunities without reapplying for new financing each time.

Commercial Real Estate Loans

Commercial real estate loans are designed for purchasing, developing, or refinancing business properties. These loans typically come with terms between 5 and 20 years, although amortization schedules (how the loan is paid down) can stretch up to 25 years.

Expect to make a substantial down payment, often 20–25%, and to pledge the property itself as collateral.

Best for: Buying office buildings, warehouses, retail spaces, or other commercial properties.

Equipment Loans

An equipment loan is specifically tailored for businesses needing to purchase heavy machinery, vehicles, computers, or other large equipment.

The equipment being financed usually serves as collateral, reducing the risk for the lender. Loan terms generally align with the equipment’s expected lifespan, usually up to 10 years.

Best for: Acquiring essential tools and technology without draining working capital.

SBA Loans

Backed by the U.S. Small Business Administration, SBA loans offer some of the most favorable terms available to small business owners.

SBA 7(a) loans, for example, can fund up to 10 years for working capital or equipment purchases, and up to 25 years for real estate projects.

While the approval process is often more document heavy and slower, SBA loans typically come with lower interest rates and smaller down payment requirements than conventional bank loans.

Best for: Entrepreneurs needing affordable, long term financing but willing to navigate a more detailed application process.

Short Term/Bridge Loans

Short term and bridge loans are designed for speed. They offer quick cash infusions with repayment periods from just a few months to 18 months.

Rates are often higher than other loan types, reflecting the lender’s greater risk, but when timing is critical, these loans can be a lifesaver.

Best for: Covering urgent expenses, bridging the gap between financing rounds, or flipping real estate investments.

Key Commercial Loan Terms and Concepts

Term | Definition/Explanation |

Principal | The original amount of money borrowed from the lender, not including interest or fees. |

Interest Rate | The cost of borrowing the principal, usually expressed as an annual percentage rate (APR). Rates can be fixed (stay the same) or variable (fluctuate over time). |

Amortization | The gradual repayment of a loan over time through scheduled payments that include both principal and interest. |

Collateral | An asset pledged to the lender to secure the loan. If the borrower defaults, the lender can seize the collateral (e.g., real estate, equipment). |

Loan to Value (LTV) | A ratio comparing the loan amount to the appraised value of the asset being financed. Lenders use this to assess risk, lower LTVs are less risky. |

Loan Agreement | A legal contract outlining the loan’s terms, repayment schedule, covenants, conditions, and consequences of default. |

Debt Service | The total cash required to cover loan payments, including principal and interest, typically calculated on a monthly or annual basis. |

Maturity | The date when the loan’s final payment is due, at which point the entire outstanding balance must be paid in full. |

Default | Failure to meet the repayment terms outlined in the loan agreement, often leading to penalties, legal action, or asset seizure. |

Guarantor | An individual or entity that agrees to repay the loan if the borrower fails to meet their obligations. |

Prepayment Penalty | A fee some lenders charge if a borrower pays off the loan early, compensating the lender for lost interest income. |

Personal Guarantee | A pledge by a business owner to personally repay the loan if the business cannot, putting personal assets at risk. |

Typical Loan Terms by Product

Loan Type | Typical Term Length | Common Interest Rate Range | Collateral Required |

Term Loan | 1–10 years (up to 25 for real estate) | 3%–36% | Often required (real estate, equipment) |

Line of Credit | 6 months–5 years | 10%–99% | Sometimes required, especially for larger lines |

SBA 7(a) Loan | Up to 10 years (25 for real estate) | 6%–13% | Yes, typically business assets or real estate |

Equipment Loan | Up to 10 years | 6%–36% | Equipment itself serves as collateral |

Commercial Real Estate | 5–20 years (amortization up to 25 years) | 3.5%–5% (as of 2024) | Property being financed |

Bridge/Short Term Loan | 3–18 months | Higher (varies by lender) | Yes, often property or assets |

Typical Requirements for Approval

- Good Credit

Most lenders require strong credit histories. Business owners should aim for a personal credit score above 680, with business credit profiles showing timely payments and low debt levels. - Financial Statements

Expect to submit tax returns, profit and loss statements, balance sheets, and sometimes cash flow projections. These documents show the business’s financial health and ability to repay. - Collateral

Many commercial loans are secured. Lenders often require physical or financial assets, such as real estate, inventory, or equipment, to back the loan. - Down Payment

Particularly for real estate and equipment loans, lenders may require a 10%–25% down payment. The larger the down payment, the less risk the lender takes on, and the better the terms you might receive. - Time in Business

Most lenders prefer businesses with at least 1 to 2 years of operating history. Startups may need to apply through specialized lenders or back their loans with stronger personal guarantees.

Common Fees

When taking out a commercial loan, the interest rate isn’t the only cost to consider. Here are some common fees that can affect your bottom line:

Origination Fee

This is a one time fee charged by the lender for processing and approving your loan application. It typically ranges from 0.5% to 3% of the total loan amount. Think of it as the lender’s “admin fee” for setting everything up.

Appraisal Fee

For loans backed by property or equipment, lenders will require an independent appraisal to determine the fair market value. Fees vary depending on the complexity and asset type but typically run between $300 to $2,000.

Legal/Documentation Fees

Preparing loan documents, reviewing contracts, and ensuring regulatory compliance often involves legal professionals. These fees can be charged as flat rates or hourly, depending on the lender’s process and the complexity of the deal.

Prepayment Penalty

Some loans come with a prepayment penalty, which is a fee for paying off your loan early. While it may seem counterintuitive, lenders use this to recover some of the interest they lose when you pay ahead of schedule. Always check for this clause before signing.

Final Thoughts: Navigate Commercial Loans Like a Pro

Understanding typical commercial loan terms isn’t just about knowing what you're signing, it's about negotiating better deals, avoiding costly surprises, and building smarter financial strategies for your business’s future.

Here’s what to remember:

- There’s no one size fits all loan. Different goals call for different products, term loans, lines of credit, real estate financing, and beyond.

- Key terms like collateral, amortization, and prepayment penalties matter. They directly impact your costs, obligations, and flexibility.

- Your financial profile matters. Lenders will scrutinize your credit, financial statements, and time in business, so come prepared.

- Fees add up. Always factor in origination, appraisal, and legal fees, not just the headline interest rate.

By mastering these commercial loan fundamentals, you're not just taking on debt, you're leveraging financial tools to grow your business with confidence.