Navigating the Complex Financial World of U.S. Canada Dual Residency

Relocating from the United States to Canada is more than a lifestyle change, it’s a financial transformation. For Americans moving to Vancouver , a city known for its quality of life and global culture, the transition brings both opportunity and complexity. Cross-border taxation, investment reporting, and retirement coordination can become traps for the unprepared.

That’s why Canada-U.S. Tax Planning isn’t just helpful, it’s essential. Proper Cross-Border Transition Planning ensures that Americans living in Canada can manage wealth efficiently, minimize double taxation, and stay compliant with both the IRS and the Canada Revenue Agency (CRA).

In this comprehensive guide, we’ll explore how an experienced cross-border financial advisor helps minimize tax liabilities, protect assets, and align long-term financial goals between two tax regimes.

1. Why Vancouver Attracts So Many Americans

Economic and Lifestyle Appeal

Vancouver offers a dynamic mix of cosmopolitan culture, natural beauty, and proximity to the U.S. West Coast. For entrepreneurs, retirees, and professionals, it’s often a seamless blend of business opportunity and outdoor living.

Growing Trend of Americans Relocating North

Post-pandemic, thousands of Americans have sought the stability of Canadian residency, access to universal healthcare, and a favorable lifestyle environment. Many come from California, Washington, and New York, states with high income taxes, hoping for a fresh start in British Columbia.

But moving north doesn’t mean leaving the IRS behind. U.S. citizens are taxed on worldwide income, even when residing abroad. This reality makes Canada-U.S. Tax Planning a cornerstone of any financial strategy for Americans living in Canada.

2. The Challenge: Two Tax Systems, One Individual

Dual Tax Residency Complications

Upon establishing Canadian residency, an American must navigate both countries’ tax systems. Each has distinct definitions of residency, taxable income, and allowable credits.

- Canada taxes residents on worldwide income starting from their date of arrival.

- The U.S. taxes its citizens regardless of where they live, unless they formally renounce citizenship.

This overlap often results in double reporting, and potential double taxation, unless the transition is carefully planned.

Common Pain Points for Cross-Border Taxpayers

- Overlapping Income Tax – Earnings may be taxed in both jurisdictions.

- Complex Foreign Account Reporting (FBAR and FATCA) – U.S. citizens must report Canadian financial accounts exceeding $10,000.

- Investment Misalignment – Canadian mutual funds can trigger punitive U.S. taxation under PFIC rules.

- Retirement Account Conflicts – RRSPs, IRAs, and 401(k)s follow different tax treatments in each country.

- Estate and Gift Tax Exposure – Cross-border inheritance planning often gets overlooked until it’s too late.

These challenges require coordination across accounting, financial, and legal disciplines, exactly where Cross-Border Transition Planning becomes invaluable.

3. Understanding the Canada-U.S. Tax Treaty

The Framework for Avoiding Double Taxation

The Canada-U.S. Tax Treaty exists to ensure fairness and prevent income from being taxed twice. It defines residency tie-breaker rules, tax credit coordination, and which country has primary taxing rights for specific income types.

Key provisions include:

- Article IV – Residency determination (the “tie-breaker” test).

- Article XVIII – Treatment of pensions and retirement savings.

- Article XXIV – Elimination of double taxation through foreign tax credits.

A cross-border financial advisor interprets how these treaty articles apply to your unique situation, optimizing deductions, timing income recognition, and structuring accounts strategically.

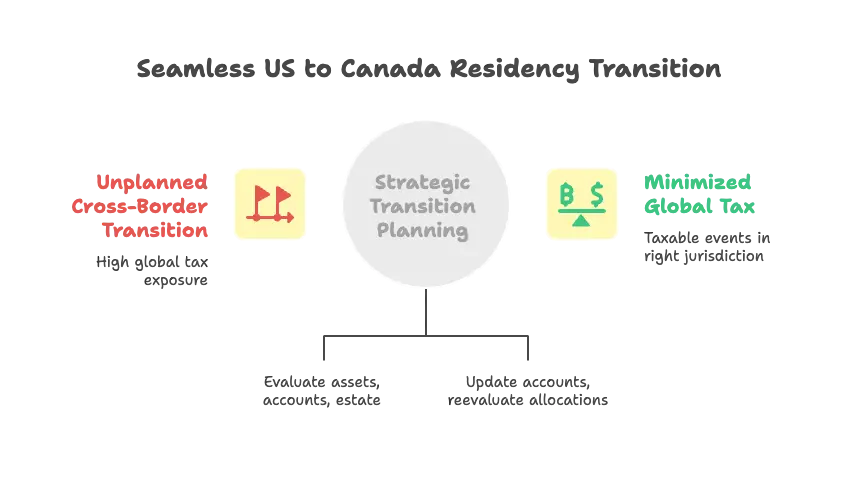

4. Cross-Border Transition Planning: The Foundation of Success

Transitioning from U.S. to Canadian residency demands more than simply updating your address. It requires synchronized planning across tax, investment, and estate dimensions.

A. Pre-Move Planning

Before relocating, Americans should evaluate:

- Capital Gains Realization: Selling appreciated U.S. assets before becoming a Canadian resident may reset cost bases.

- Retirement Account Positioning: Deciding whether to convert 401(k)s to IRAs, or roll over pensions.

- Estate Restructuring: Aligning wills and trusts to reflect Canadian domicile laws.

- Business Ownership Adjustments: Determining the most tax-efficient way to continue operating or drawing income from a U.S. entity.

B. Post-Move Adjustments

After arrival:

- Update all investment and banking accounts for tax residency status.

- Reevaluate asset allocations under Canadian securities laws.

- Optimize foreign tax credits under the treaty.

- Plan for ongoing U.S. compliance (Form 1040, FBAR, FATCA).

C. Strategic Goal: Minimize Global Tax Exposure

Effective Cross-Border Transition Planning synchronizes the U.S. and Canadian calendars, ensuring taxable events occur in the right jurisdiction at the right time.

5. How a Cross-Border Financial Advisor Bridges Two Worlds

An experienced advisor acts as both navigator and translator between two financial systems. Their expertise lies in harmonizing taxation, investment, and estate strategies.

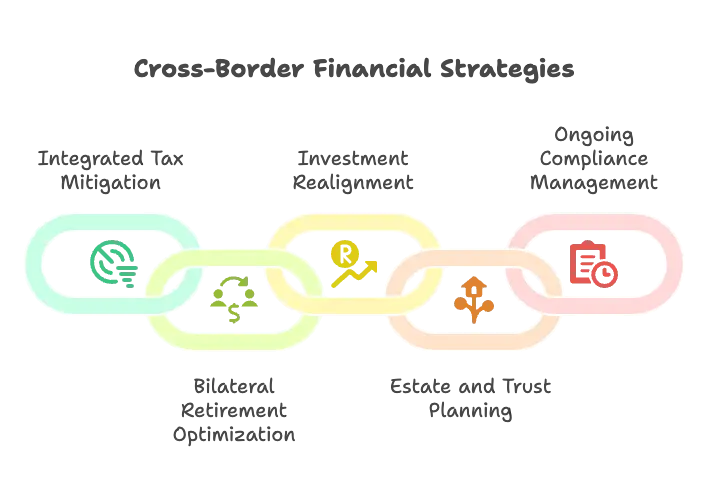

Key Capabilities Include:

- Integrated Tax Mitigation

- Use of the foreign earned income exclusion (FEIE) and foreign tax credits.

- Strategic Roth conversions before moving to Canada.

- Avoidance of PFIC pitfalls through proper investment structuring.

- Bilateral Retirement Optimization

- Coordinating RRSP, IRA, 401(k), and Roth accounts under treaty provisions.

- Advising on when and how to withdraw from each to minimize taxation.

- Investment Realignment

- Restructuring portfolios for cross-border tax efficiency.

- Avoiding Canadian mutual funds with PFIC exposure and selecting treaty-friendly ETFs.

- Estate and Trust Planning

- Aligning wills and trusts with both Canadian and U.S. jurisdictions.

- Managing estate tax exposure for Americans holding U.S.-situs assets.

- Ongoing Compliance Management

- Coordinating annual filings across two tax systems.

- Managing reporting obligations like FBAR and Form 8938.

Through this coordination, the advisor ensures that every dollar earned, saved, or invested is optimized for both systems.

6. Tax Minimization Strategies for Americans Living in Vancouver

1. Optimize Timing of Residency

Determining your date of departure from the U.S. and date of arrival in Canada has significant tax implications. The goal is to avoid overlapping periods where both countries claim residency.

2. Utilize the Foreign Tax Credit (FTC)

Under the treaty, U.S. taxpayers can claim a credit for Canadian taxes paid, reducing double taxation. However, proper classification of income types, passive, general, or earned, is essential for accurate calculation.

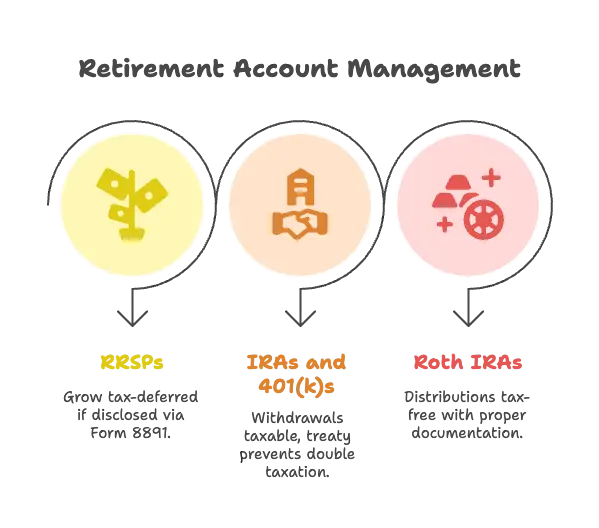

3. Manage Retirement Accounts Proactively

- RRSPs: Under Article XVIII(7), these can grow tax-deferred for U.S. purposes if properly disclosed via Form 8891 or successor reporting.

- IRAs and 401(k)s: Withdrawals are taxable in the country of residence but coordinated under the treaty to prevent double taxation.

- Roth IRAs: If structured pre-move, distributions can remain tax-free in both countries with proper documentation.

4. Avoid PFIC Traps

Canadian mutual funds and ETFs are classified as Passive Foreign Investment Companies (PFICs) by the IRS, which can result in punitive taxation unless handled through a QEF or MTM election.

A cross-border financial advisor helps reallocate these into U.S.-compliant, treaty-friendly investments before arrival.

5. Structure Real Estate Ownership Efficiently

For Americans moving to Vancouver, real estate planning requires attention to both capital gains and currency exchange considerations. Selling U.S. property before residency change or structuring ownership in Canadian property through tax-efficient vehicles can preserve long-term equity.

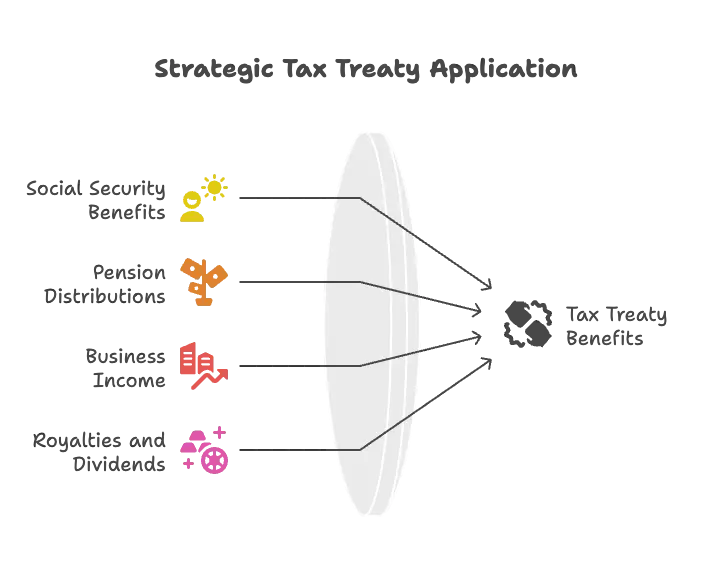

6. Leverage Tax Treaty Provisions

Strategically applying treaty benefits can prevent double taxation on:

- Social Security benefits

- Pension distributions

- Business income

- Royalties and dividends

7. Coordinating Business and Self-Employment Income

Many Americans continue to operate U.S.-based businesses after moving to Canada. This requires special handling to avoid permanent establishment issues or misclassification of income.

Cross-Border Structuring Options

- Maintain a U.S. LLC but ensure management control is not conducted in Canada.

- Consider incorporation in Canada for business activities performed there.

- Use intercompany agreements to allocate income properly between jurisdictions.

Avoiding Double Social Security Contributions

Through the U.S.–Canada Totalization Agreement, individuals can avoid paying into both countries’ pension systems simultaneously by determining the primary system under which they contribute.

8. Real-World Example: A Case Study in Tax Optimization

The Situation

David and Laura, a married couple from Seattle, relocated to Vancouver in 2024 for Laura’s work in biotech. They kept their Seattle home as a rental property and held significant 401(k) and IRA assets.

The Challenge

Without guidance, they risked:

- Double taxation on rental income

- PFIC exposure through Canadian mutual funds

- Missed credits for Canadian taxes paid

The Solution

Working with a cross-border financial advisor, they:

- Converted U.S. mutual funds into ETFs that qualified under PFIC exemptions.

- Filed under the Canada-U.S. Tax Treaty to claim credits for Canadian taxes.

- Implemented Roth conversions pre-move to minimize future taxable income.

- Structured their rental property for efficient depreciation and reporting.

The Result

They reduced global tax exposure by 27%, avoided PFIC penalties, and synchronized their retirement drawdown strategy across both countries, achieving true cross-border tax harmony.

9. Estate Planning for Americans Living in Canada

Understanding Dual Jurisdiction Wills

U.S. citizens in Canada should have wills that align with both legal systems. Canadian provinces may not automatically recognize U.S. wills, and vice versa.

A cross-border financial advisor often works alongside legal counsel to:

- Draft separate but coordinated wills for each jurisdiction.

- Minimize estate taxes on U.S.-situs assets (e.g., real estate or securities).

- Ensure smooth transfer of assets across borders.

Estate Tax Thresholds and Planning

- The U.S. estate tax exemption (as of 2025) is approximately USD $13.61 million but may revert to lower levels after 2026.

- Canada has no estate tax but treats capital gains at death as a deemed disposition.

Strategic coordination avoids unintended consequences such as double inclusion of asset values or lost tax credits.

10. Managing Currency and Investment Risk

Exchange Rate Volatility

The CAD/USD exchange rate can fluctuate significantly, impacting investment returns and retirement distributions. Advisors may recommend:

- Holding diversified currency exposure within portfolios.

- Timing major transactions (like withdrawals or property sales) based on favorable exchange conditions.

Tax Implications of Currency Gains

The IRS treats currency gains over $200 as taxable events, even for personal transactions. Managing currency conversion efficiently reduces unnecessary tax exposure.

11. Retirement Planning Across Borders

Harmonizing Pension and Social Security Benefits

Under the U.S.–Canada Totalization Agreement, time worked in each country can be combined to qualify for benefits under either system. However, payout taxation depends on residency status and treaty coordination.

Cross-Border Drawdown Strategies

Advisors structure withdrawals from:

- RRSPs for early retirement income taxed in Canada.

- IRAs and 401(k)s with U.S. withholding adjusted to treaty rates (typically 15%).

- Roth IRAs for tax-free distributions if properly pre-established.

Effective drawdown timing can reduce cumulative lifetime taxation by optimizing where income is recognized.

12. Philanthropy and Charitable Giving

Donations made to Canadian charities are not automatically deductible on U.S. returns unless the organization has special status under the treaty. Cross-border advisors identify eligible charities or coordinate giving through U.S.-based donor-advised funds that align with Canadian tax credit rules.

13. How Vancouver’s Tax Landscape Interacts with U.S. Rules

Provincial Tax Considerations

British Columbia levies its own provincial income tax on top of federal rates, ranging from 5% to 20.5%. Combined with federal tax, top earners can face marginal rates exceeding 50%.

When integrated with U.S. tax obligations, this underscores the importance of maximizing foreign tax credits and planning withdrawals strategically.

Vancouver Real Estate Taxation

For Americans investing in property:

- Speculation and Vacancy Tax applies to underused properties.

- Capital Gains Tax applies on disposition, coordinated with U.S. capital gains.

- Principal Residence Exemption may apply under Canadian law but not always under U.S. rules.

14. The Role of Technology in Cross-Border Wealth Management

Modern cross-border financial advisors employ digital platforms that synchronize portfolio data, tax projections, and compliance workflows across jurisdictions.

These systems:

- Consolidate investment reporting in both currencies.

- Automate FBAR and FATCA data preparation.

- Model scenarios for after-tax returns under different treaty interpretations.

For Americans living in Canada, technology-enabled planning enhances transparency and control over complex, multi-jurisdictional assets.

15. Selecting the Right Cross-Border Financial Advisor

What to Look For

- Dual Licensing – Registered in both the U.S. (FINRA/SEC) and Canada (IIROC or provincial regulators).

- Experience with Expat Clients – Proven history advising U.S. citizens in Canada.

- Collaborative Network – Partnerships with cross-border accountants and estate attorneys.

- Transparent Fee Structure – Avoiding commission conflicts ensures objective advice.

- Holistic Financial Planning Approach – Integration of tax, investment, and estate disciplines.

Questions to Ask

- How do you coordinate filings between the IRS and CRA?

- What’s your experience managing PFIC exposure?

- How do you structure portfolios to avoid double taxation?

- Can you provide ongoing compliance and reporting support?

16. The Long-Term Benefits of Professional Cross-Border Guidance

Financial Clarity

By maintaining a synchronized approach, Americans in Vancouver gain visibility into how each financial decision impacts both tax systems.

Reduced Tax Liability

Coordinated planning can cut cumulative tax exposure by aligning income timing, residency classification, and investment structuring.

Regulatory Compliance

Avoiding penalties from the IRS or CRA requires constant vigilance. A cross-border advisor ensures full compliance through proactive reporting and monitoring.

Peace of Mind

Ultimately, Cross-Border Transition Planning transforms uncertainty into confidence, allowing expatriates to focus on life, family, and opportunity rather than tax code nuances.

17. The Bottom Line: Strategic Planning Means Sustainable Wealth

For Americans moving to Vancouver, the journey is both exciting and intricate. The interplay between the U.S. and Canadian financial systems requires more than generic advice. It demands an expert versed in Canada-U.S. Tax Planning, someone who can coordinate your transition, safeguard assets, and legally minimize your tax obligations.

A qualified cross-border financial advisor acts as your strategic partner, bridging nations, tax codes, and financial goals. Through pre-move preparation, ongoing compliance, and holistic portfolio alignment, they ensure you enjoy the benefits of dual residency without the burden of double taxation.

Whether you’re planning a relocation or have already settled in British Columbia, proactive Cross-Border Transition Planning today secures your financial freedom tomorrow.

Leave a comment

Your email address will not be published. Required fields are marked *