In 2025, your “banking accounts” is really part of your tech stack. Founders expect instant payouts, clean APIs, automated bookkeeping, and support that moves at startup speed. Novo and Mercury* see what each platform does at a glance, including checking, savings/yield, invoicing, ATM access, integrations, cards, international, and startup perks. Then scan Fees & Pricing and Customer Experience for the fine print that affects real costs and support. We’ll highlight unique advantages and major drawbacks on both sides, and close with a practical verdict that tells you exactly who should choose Novo and who should choose Mercury. Skim the table, read the sections that matter to your stage, and jump to the verdict when you’re ready to decide.

Core Offerings & Features

Feature | Novo | Mercury |

Main User | Small businesses, freelancers, sole proprietors welcome. | Tech-forward startups and scaling companies; generally not available to trusts or public-traded companies. |

Checking | $0/mo checking; free ACH and mailed checks; incoming wires free; domestic wire sending available for eligible accounts; international via Wise. | $0/mo checking; free ACH; free domestic wires and free USD international wires. |

Savings | No separate savings; uses “Reserves” sub-accounts for budgeting/auto-allocations. | Savings plus Mercury Treasury** for yield/cash management ($350k minimum account balance requirement). |

Invoicing | Built-in, unlimited invoicing with reminders and multiple payment options. | Built-in invoicing; advanced features like recurring/branding live in paid tiers. |

ATM Access | Reimburses ATM fees up to $7/month. | Debit card supports ATM withdrawals; no cash deposits; ATM/operator fees may apply. |

Integrations | QuickBooks, Xero, Stripe, Square, Shopify, and more; Boost for faster Stripe payouts. | Robust developer API + accounting/bill-pay workflows; easy app connections (e.g., Plaid). |

Startup Perks | Partner discounts on popular tools; Stripe perk ($5k fee-free card processing). | Investor Database, large perk marketplace (AWS/Google Cloud credits) |

Card Access | Physical + virtual Mastercard debit. | Physical/virtual debit and IO credit card*** with unlimited 1.5% cashback (on approval). |

International | US-based accounts; send international payments via built-in Wise integration. | Pay in 40+ local currencies with a flat 1% FX fee; USD international wires free. |

If you found this guide helpful, consider supporting the blog by using my affiliate link when joining Mercury. It won’t cost you anything extra, and it helps me keep creating free content.

Customer Experience

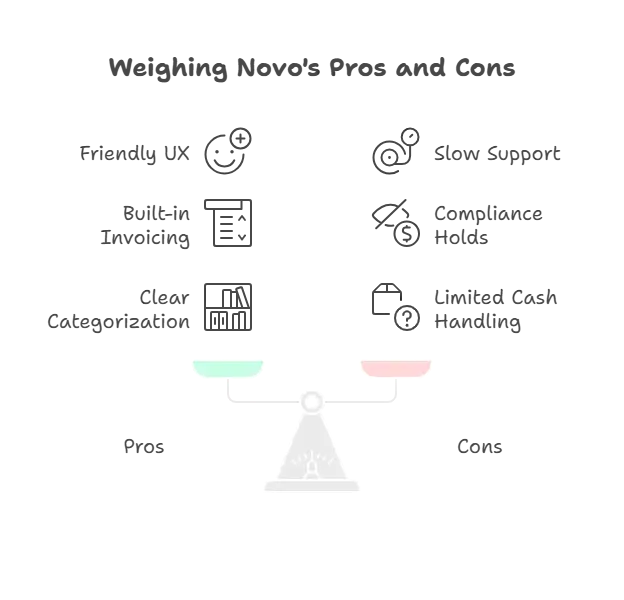

Novo

Pros:

- Friendly, approachable UX, easy for first-time business owners.

- Built-in invoicing and quick Stripe payouts reduce tool sprawl.

- Clear categorization and “Reserves” make cash organization simple.

Cons:

- Support can feel slow during peak times; email-first responses.

- Occasional compliance reviews/holds can disrupt cash flow.

- Limited cash handling; no interest-bearing savings.

Common themes: Ideal for freelancers/solo LLCs that value simplicity and perks; less loved by high-volume operators who need white-glove support or advanced treasury tools.

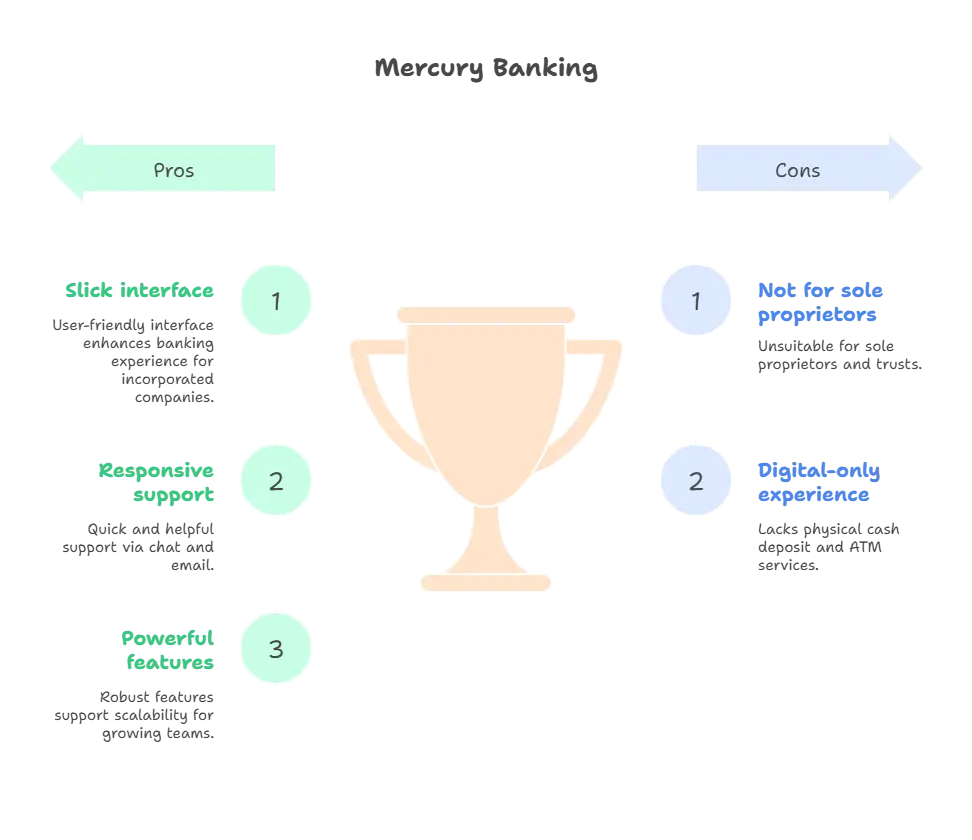

Mercury

Pros:

- Slick interface, fast onboarding for incorporated companies, strong founder community cred.

- Responsive chat/email support; good documentation for APIs and workflows.

- Powerful features (multi-user controls, rules, treasury) that scale smoothly as teams grow.

Cons:

- Not built for trusts or publicly-traded companies.

- No cash deposits; 100% digital experience.

Common themes: A favorite among tech-forward teams that want automation, better yield options, and startup ecosystem perks; less of a fit if you need branch/ATM-centric banking.

Mobile/App Experience

- Onboarding: Both are app-centric with quick KYC. Novo feels more “consumer-simple” for first-time founders; Mercury’s flow is streamlined for C-corps/LLCs with team roles.

- Ease of use: Clear dashboards and fast search; Novo prioritizes invoicing and expense basics, Mercury emphasizes workflows, approvals, and API-driven automation.

Suitability by maturity:

- Early/solo stage: Novo’s simplicity and invoicing tools shine.

- Growing/startup stage: Mercury’s multi-user controls, developer tooling, and Treasury** features fit scaling teams.

Customer Experience

Novo: pros/cons & common themes

- Pros: Approachable UX for first-time owners; built-in invoicing and Reserves keep cash tidy; few core fees.

- Cons: Mixed support sentiment, slow replies and limited live support; no cash deposits; some complaints about holds/closures.

- What reviewers repeat: Great for freelancers/solo LLCs that want simplicity and invoicing; frustration spikes when urgent, high-stakes support is needed.

Mercury: pros/cons & common themes

- Pros: Clean, fast interface; responsive chat/email support; strong for teams with roles, rules, and API-friendly workflows.

- Cons: Not built for trusts or publicly-traded companies; fully digital (no cash deposits/branching).

- What reviewers repeat: Favored by startup founders for ease, automation, and scaling features; occasional edge cases with reviews/closures appear in public forums and complaints.

Mobile/App Experience: onboarding, ease, fit by stage

- Onboarding: Both run quick, app-centric KYC; Mercury’s flow assumes an incorporated company and the right documents.

- Ease of use: Novo keeps day-one tasks simple (invoicing, categorization); Mercury leans into multi-user controls, approvals, and web-first workflows.

- App ratings (signal of day-to-day UX): Mercury iOS app shows 4.9/5 across regions; Novo’s mobile apps are typically 4.7 – 4.8/5 on iOS and 4.6 – 4.7/5 on Android in recent roundups.

Fit by maturity:

- Early/solo: Novo’s simplicity + invoicing reduce tool sprawl.

- Scaling/team: Mercury’s approvals, roles, and API/documentation suit growing ops.

Unique Advantages

Why Entrepreneurs Choose Novo

- Free, built-in invoicing (unlimited) with payment links, no extra software needed.

- Cash-flow helpers: faster Stripe payouts via Boost + Reserves sub-accounts to auto-set aside taxes/payroll.

- Real-world access: physical/virtual debit card and ATM fee reimbursements for on-the-go cash needs.

- Founder-friendly setup: welcomes freelancers/sole props; plug-and-play with QuickBooks, Xero, Shopify, Stripe.

Why Entrepreneurs Choose Mercury

- Scale-ready operations: free domestic and USD international wires, multi-user roles, and approval workflows.

- Make idle cash work: Mercury Treasury**, by Mercury Advisory, helps high-growth startups optimize idle cash through an automated investment strategy designed to balance liquidity, yield, and risk.

- Developer-first DNA: robust API/webhooks to automate payouts, reconciliation, and custom workflows.

- Startup ecosystem perks: investor database, and big-ticket cloud credits.

Major Drawbacks

Novo

- No interest-bearing savings: “Reserves” help with budgeting but don’t earn yield.

- Cash handling limits: No cash deposits; ATM access exists but reimbursements are limited.

- Support variability: Mixed reports of slow responses and occasional compliance-related account holds/closures.

Mercury

- Eligibility limits: Generally not available to trusts or publicly-traded companies.

- No cash banking: No cash deposits and no ATM/branch focus, 100% digital.

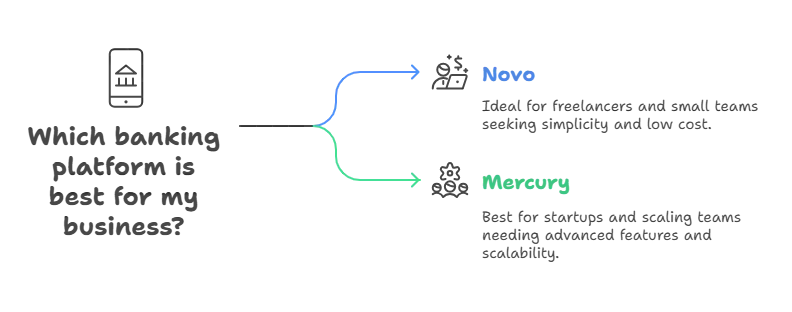

Verdict: Who Wins for Entrepreneurs?

Short verdict: If you’re a freelancer or very small team that wants simple, low-cost banking with built-in invoicing and easy cash access, Novo is the better everyday fit. If you’re a startup or scaling company that needs multi-user controls, automation, free wires, higher insurance, and yield on idle cash, Mercury delivers more leverage.

Recommendations by business type

If you found this guide helpful, consider supporting the blog by using my affiliate link when joining Mercury. It won’t cost you anything extra, and it helps me keep creating free content.

- Freelancers / Small Teams: Pick Novo: straightforward setup for sole props/LLCs, unlimited invoicing, and practical ATM access to keep operations lean.

- Startups / Scaling Teams: Pick Mercury: role-based controls, API-first workflows, treasury/yield options, and strong founder perks make it scale-ready.

*Mercury is a fintech company, not an FDIC-insured bank. Checking and savings accounts are provided through our bank partners Choice Financial Group, Column N.A., and Evolve Bank & Trust; Members FDIC. Deposit insurance covers the failure of an insured bank. Checking and savings account deposits may be held by sweep network banks. Certain conditions must be satisfied for pass-through insurance to apply. Learn more here.

**Mercury Treasury, offered by Mercury Advisory, LLC, an SEC-registered investment adviser, seeks to earn net returns up to 4.26% annually on your idle cash. Net return or yield provided assumes total Mercury deposits of $20M+, is accurate as of 08/11/2025, and is subject to change.

This communication does not constitute an offer to sell or the solicitation of any offer to purchase any security. Funds in Mercury Treasury are subject to investment risks, including possible loss of the principal invested, and past performance is not indicative of future results. Some of the data contained in this message was obtained from sources believed to be accurate but has not been independently verified. Please see full disclosures at mercury.com/treasury. Mercury Advisory is a wholly-owned subsidiary of Mercury Technologies.

Mercury Treasury is not insured by the FDIC. Funds in Mercury Treasury are not deposits or other obligations of Choice Financial Group, Column N.A., or Evolve Bank & Trust, and are not guaranteed by Choice Financial Group, Column N.A., or Evolve Bank & Trust.

***The IO Card is issued by Patriot Bank, Member FDIC, pursuant to a license from Mastercard®. To receive cash back, your Mercury accounts must be open and in good standing, meaning they cannot be suspended, restricted, past due, or otherwise in default.

Leave a comment

Your email address will not be published. Required fields are marked *