Leasing a car with bad credit can feel like trying to buy champagne on a beer budget, most people assume it’s just not going to happen. Dealerships check your credit, lenders scrutinize your payment history, and the internet is full of horror stories. But here’s the truth: yes, you can lease a car with bad credit. You’ll just need to understand how the process works, what challenges to expect, and how to stack the odds in your favor. In this guide, we’ll break down exactly how to lease a vehicle even if your credit score isn’t perfect, and how to make smarter moves along the way.

Can You Lease a Car With Bad Credit?

The short answer is yes, but it’s definitely harder.

Leasing a car with bad credit is possible, but you’ll likely face a few bumps in the road. Unlike buyers with excellent credit, you may not walk into a dealership and drive out with the latest model at a rock-bottom rate. Instead, expect to encounter:

- Higher security deposits or down payments to offset the risk for the lessor.

- Increased interest rates (known as the money factor in lease terms).

- Higher monthly lease payments, even on modest vehicles.

- Limited selection, as some dealerships restrict leasing options based on credit thresholds.

That said, there’s a surprising twist: leasing can sometimes be easier than financing a car purchase. Why? Because leases are shorter-term commitments and the vehicle is often returned before it depreciates too much, making it a lower risk for the dealership. If you can show you're financially stable now, even with a rough credit history, you might find more flexibility in leasing than you would with a traditional auto loan.

How to Lease a Car With Bad Credit: Practical Steps

If your credit is holding you back, don’t worry, there are strategic ways to increase your chances of getting approved for a lease. Here’s a step-by-step breakdown of what you can do to make leasing with bad credit more realistic:

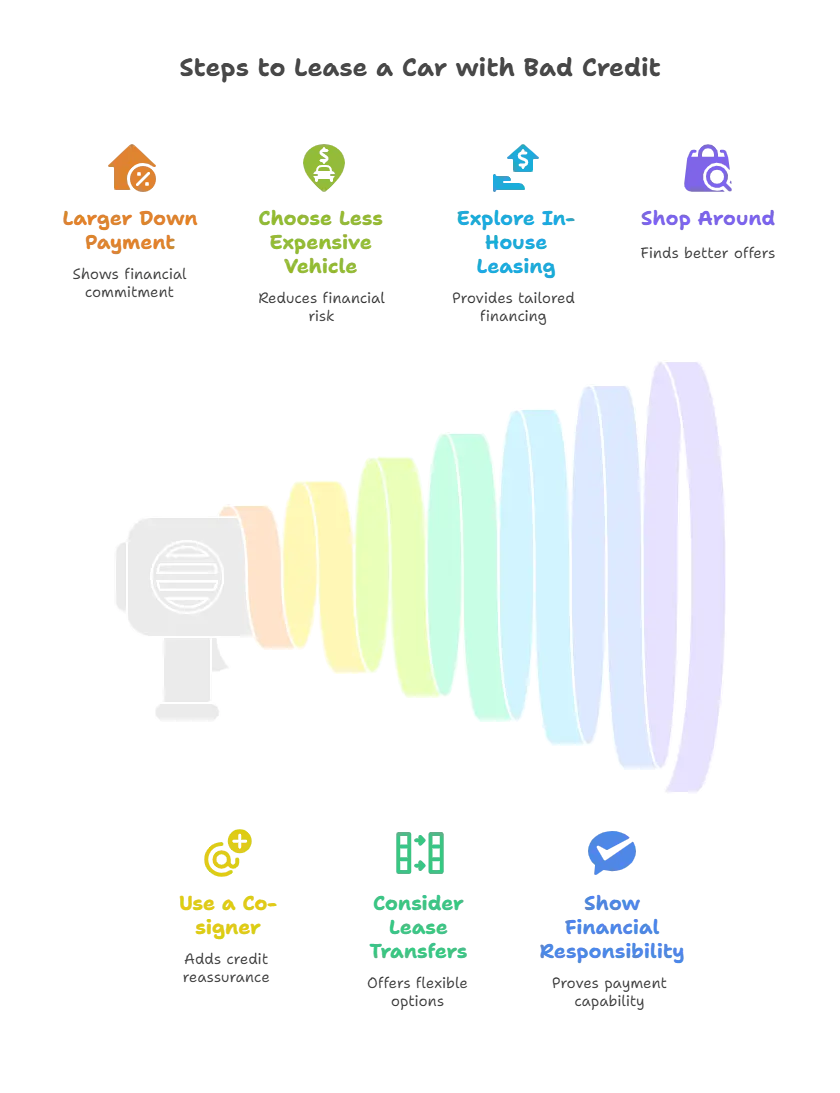

1. Consider a Larger Down Payment

Putting more money down at signing shows financial commitment and reduces the risk for the dealership. It can also help lower your monthly payments and make your application more appealing, even with a lower credit score.

2. Use a Co-signer

A co-signer with good credit can open doors that might otherwise be closed. Their credit profile adds reassurance for the lender, and it may qualify you for better lease terms, including lower interest rates.

3. Choose a Less Expensive Vehicle

Dealers are more likely to lease lower-cost models to applicants with bad credit because the financial risk is reduced. Focus on practical, reliable cars, not the flashy dream ride (at least for now).

4. Consider Lease Transfers or Assumptions

A lease transfer lets you take over someone else’s lease mid-term. These often have more flexible approval requirements, lower upfront costs, and shorter commitments, ideal if you’re rebuilding credit.

5. Explore In-House/“Buy Here, Pay Here” Leasing Programs

Some dealerships offer internal lease financing tailored to people with credit issues. Be cautious, these deals often come with steep interest rates and limited car selection, but they can be a viable option if other paths aren’t working.

6. Show Proof of Financial Responsibility

If your credit score doesn’t reflect your current financial situation, bring documentation. Steady income, recent pay stubs, bank statements, and utility bill history can help prove you’re capable of making regular lease payments.

7. Shop Around and Compare Offers

Every dealership and lender has different approval standards. Cast a wide net, what one dealer turns down, another might approve. Comparison shopping can uncover hidden opportunities and better terms.

Helpful Tips to Improve Your Approval Odds

Before you step onto a dealership lot or fill out an application, a little prep work can go a long way, especially when you’re dealing with a less-than-stellar credit score. Here are some fast, practical ways to improve your approval chances:

- Pay off small, manageable debts to slightly bump your credit score and lower your overall debt-to-income ratio.

- Make all current payments on time, even if it’s just the minimum. Payment history is one of the biggest factors in your credit score.

- Avoid applying for new credit in the months leading up to your lease application. Each hard inquiry can ding your score and signal risk to lenders.

- Keep your oldest credit accounts open, even if you’re not actively using them. A long credit history works in your favor.

These small moves help build lender confidence, and they can mean the difference between a rejection and a handshake.

Will Leasing Help My Credit?

Absolutely, if you handle it the right way. Leasing a car and making on-time monthly payments is one of the most effective ways to rebuild your credit. Most leasing companies report to the major credit bureaus, which means each timely payment strengthens your payment history and credit profile.

Think of it as a credit recovery tool on wheels: as long as you stay consistent, responsible leasing can help pave the road to better credit and easier financing options in the future.

Alternatives to Leasing

If leasing still feels out of reach, or just isn’t the right fit for your situation, don’t worry. There are other routes to getting behind the wheel, even with bad credit:

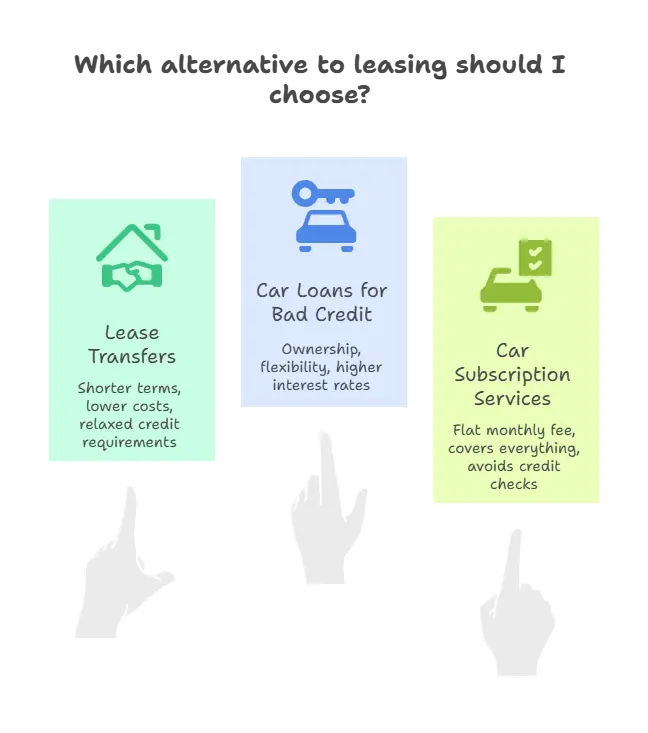

- Lease Transfers

Sites like Swapalease or LeaseTrader let you take over someone else’s lease. These typically come with shorter terms, lower upfront costs, and more relaxed credit requirements.

- Car Loans for Bad Credit

Some lenders specialize in auto loans for people with poor credit. The interest rates may be higher, but you’ll own the vehicle outright and have more flexibility in vehicle choice.

- Car Subscription Services or Car-Sharing Models

Companies like Zipcar, Flexdrive, or even traditional automakers now offer car subscription services. You pay a flat monthly fee that covers everything, maintenance, insurance, and the car itself. It's a flexible, short-term alternative that avoids credit checks entirely in some cases.

Final Takeaway

Leasing a car with bad credit isn’t a dead end, it’s just a detour that requires a bit more planning and flexibility. With the right preparation, a larger down payment, and smart choices like co-signers or lease transfers, you can absolutely get approved and hit the road.

More importantly, a lease can be more than just transportation, it can be a stepping stone to rebuilding your credit, proving your reliability, and opening doors to better financial opportunities down the line. Stay proactive, stay informed, and remember: your credit score doesn’t define your ability to move forward.

Leave a comment

Your email address will not be published. Required fields are marked *